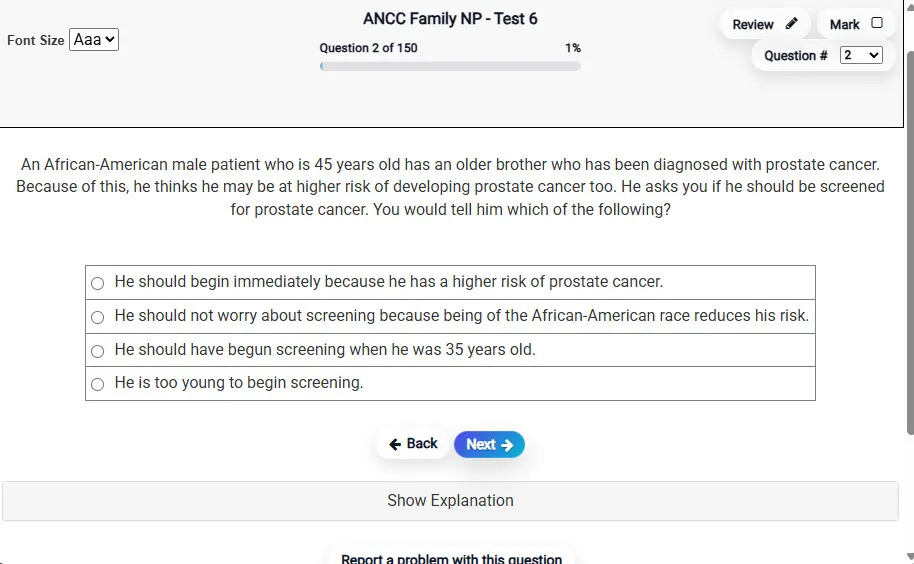

Answer Question Screen

- Clean multiple-choice interface with progress bar.

- Mark for review feature.

- Matches real test pacing.

Strike while the savings are hot! Use promo code FlashSale at checkout for 12% off any Exam Edge test or bundle. Hurry—the clock is ticking!

** All Prices are in US Dollars (USD) **

Understanding the exact breakdown of the Series 63 Uniform Securities Agent State Law Exam test will help you know what to expect and how to most effectively prepare. The Series 63 Uniform Securities Agent State Law Exam has multiple-choice questions . The exam will be broken down into the sections below:

| Series 63 Uniform Securities Agent State Law Exam Exam Blueprint | ||

|---|---|---|

| Domain Name | % | Number of Questions |

| State Securities Acts and related rules and regulations | 60% | 36 |

| Regulation of Investment Advisers - including state registered and federal covered advisers | ||

| Regulation of Investment Adviser Representatives | ||

| Regulation of Broker-dealers (e.g. - Definition - Registration - Post-Registration requirements) | ||

| Regulations of Securities and Issuers | ||

| Remedies and Administrative Provisions | ||

| Ethical practices and fiduciary obligations | 40% | 24 |

| communications with clients and prospects | ||

| compensation | ||

| client funds and securities | ||

| conflicts of interest and other fiduciary issues | ||

Everything you need to prepare with confidence—without wasting a minute.

Timed, No Time Limit, or Explanation mode.

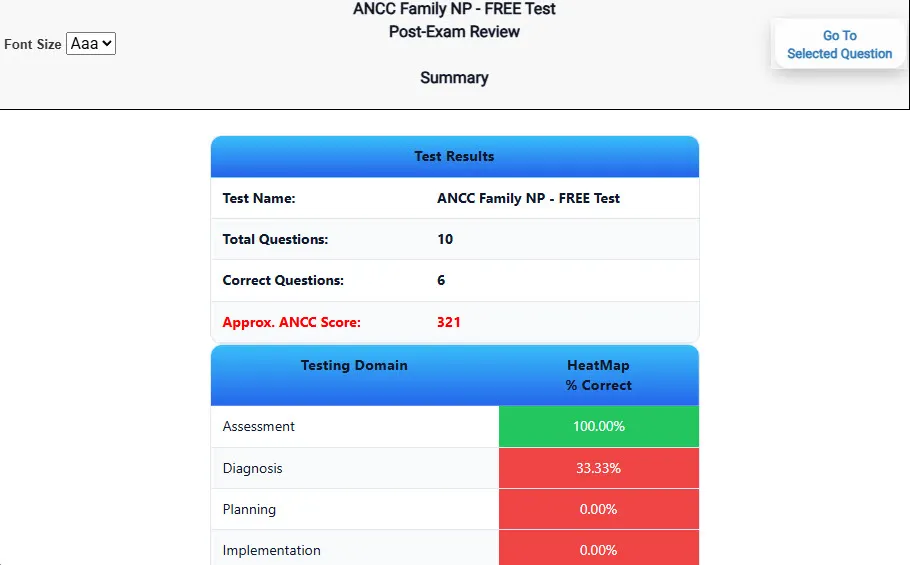

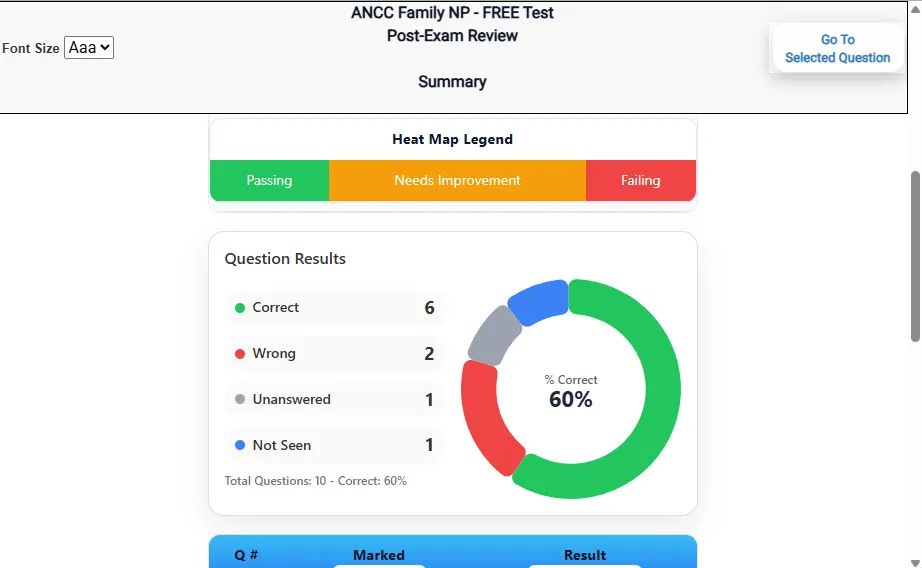

Heatmaps and scaled scores highlight weak areas.

Concise explanations emphasize key concepts.

Matches the feel of the actual exam environment.

Clean layout reduces cognitive load.

Web-based access 24/7 on any device.

Our practice tests are built specifically for the Series 63 Uniform Securities Agent State Law Exam* exam — every question mirrors the real topics, format, and difficulty so you're studying exactly what matters.

We match the per-question time limits and pressure of the actual Series exam, so test day feels familiar and stress-free.

You'll have more than enough material to master every Series 63 Uniform Securities Agent State Law Exam* concept — no repeats, no fluff.

Ordering 5 practice exams costs less than retaking the Series 63 Uniform Securities Agent State Law Exam exam after a failure. One low fee could save you both time and money.

Need to step away mid-exam? Pick up right where you left off — with your remaining time intact.

See your raw score and an estimated Series 63 Uniform Securities Agent State Law Exam score immediately after finishing each practice test.

Review correct and incorrect answers with clear, step-by-step explanations so you truly understand each topic.

We're fully accredited by the Better Business Bureau and uphold the highest standards of trust and transparency.

No software to install. Access your Series 63 Uniform Securities Agent State Law Exam* practice exams 24/7 from any computer or mobile device.

Need extra help? Our specialized tutors are highly qualified and ready to support your Series exam prep.

Preparing for your upcoming Series 63 Uniform Securities Agent State Law Exam (Series63) Certification Exam can feel overwhelming — but the right practice makes all the difference. Exam Edge gives you the tools, structure, and confidence to pass on your first try. Our online practice exams are built to match the real Series 63 Uniform Securities Agent State Law Exam* exam in content, format, and difficulty.

These Series 63 Uniform Securities Agent State Law Exam practice exams are designed to simulate the real testing experience by matching question types, timing, and difficulty level. This approach helps you get comfortable not just with the exam content, but also with the testing environment, so you walk into your exam day focused and confident.

“ The questions in the practice tests were very similar to what was on the actual FINRA Series 65 exam. I liked that you could take a timed test or take a test at my own pace with the ability to review the answers as I go. That really helped me to focus on where I needed to spend more time studying. T ...

Here is a list of alternative names used for this exam.